Secrets and Savings; what you can do about skyrocketing homeowner’s insurance rates

COLORADO SPRINGS, Colo. (KRDO) - According to data found by the S&P 500, Colorado has ranked second in the nation for rising homeowner’s insurance rates between 2018 and 2023.

This year, many homeowners reported to KRDO13 Investigates a massive spike in their homeowner’s insurance premiums, seemingly overnight.

Kimberly Bolding is one of those homeowner. She saw an 85% jump in her homeowner’s insurance rates from last year to this year, after making no claims on her home.

“My first thought was why?” Bolding, a Colorado Springs homeowner said. “I can totally understand that the economic situation going on and inflation going on. But 85% is way over."

Bolding struggles with muscular dystrophy and can not physically go to work every day. She is also a single mom, still supporting one child at home. Nevertheless, she says she’s maintained a high credit score and taken good care of her home.

In the same city, a few streets away, Luann Box is experiencing the same problem. Her homeowner’s insurance rates have been rising steadily for the last three years. This year, her bill jumped about $500.

“I'm like, Oh my God, how are we going to do this?” Box said.

Box also made no claims on her insurance and is left with two months of savings after she lost her job.

Additionally, homeowners like Box and Bolding are often left without answers as to why their rates increased so dramatically, seemingly overnight.

WHAT’S BEHIND THE RISING RATES

In 2018, Colorado Springs ranked highest in the nation for Hail Damage-related insurance claims, according to data from the State Department of Insurance. That started a six-year series of disasters, both economical and natural, that rocked the insurance industry in Colorado.

"If the insurance company does not make money, they will either raise the rates and or raise the deductibles or they'll just leave the state,” JP West, a local insurance broker said.

West went on to explain that the number of claims in the state, related to fire, hail, or wind damage means that insurance companies continually lose money in the state, forcing them to raise rates so they can afford to do business there.

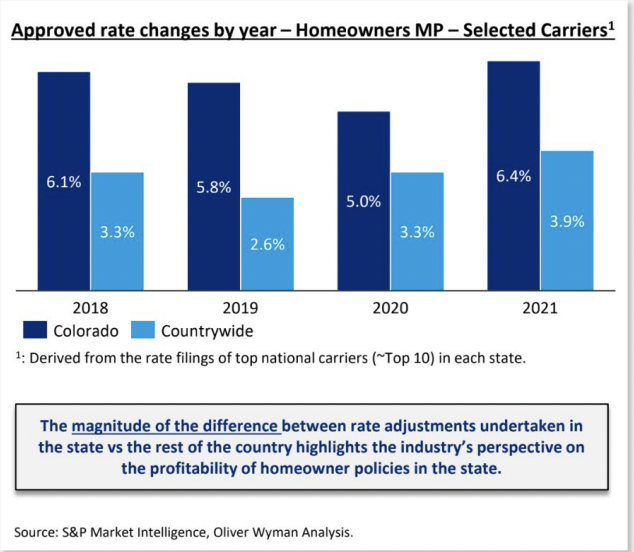

The State Department of Insurance, in an effort to mitigate the loss, has been continually approving rate increases at a higher rate than the national average, between 2018 and 2021.

However, according to West, if the DOI was not allowing for the rate increases, the market would be in a much worse place. However, the state is still working on solutions to ensure market viability.

STATE SOLUTIONS

In 2023, State Lawmakers approved the FAIR plan, a state-subsidized homeowner’s insurance plan that is for high-risk customers only, who have been denied coverage multiple times. Though the plan is in motion, the plan’s website states that coverage won’t be available until 2025.

The state has also approved multiple insurance studies in an effort to better understand how to solve the problem facing Colorado homeowners this year.

KRDO13 Investigates reached out to the State Department of Insurance to understand what they were doing about the rising rates.

“ Across the country, we are seeing insurance rates increase which is why in Colorado, we are focused on taking steps to help Coloradans save money on their insurance and boost preparedness and mitigation efforts to lower risks, such as climate change and natural disasters like fire, which increase homeowners insurance. The state continues to implement strategies to mitigate fire risk and help Coloradans protect their homes while saving people money on insurance. The state has passed and continues to implement the FAIR plan, which expands coverage for the highest-risk portions of the state.

The Colorado Division of Insurance (DOI) also developed a Toolkit for Homeowners and HOAs on Insurance - Information and FAQs. This is designed as a resource for Coloradans and homeowners experiencing challenges. “

Vincent Plymell, the State Department of Insurance

Plymell went on to detail how homeowners can tackle the problem, including tactics like shopping around for insurance and going over the coverage in their current policy to see what they can and can’t cut.

Experts like West, however, have some sneakier ways to get around Insurance company premiums.

WHAT YOU CAN DO

- Make a call to your insurance company

Sometimes something as small as asking your insurance company for a different rate can help reduce the rate at which they charge you. For Kimberly Bolding, it helped reduce her rate to lower than it was previously.

- Bundle your coverage

Bundling your coverage can help reduce your overall rate, if you pay for multiple policies at a time.

“Bundling your policies, if you carry multiple different policies for your car, your home, and even your life insurance is something that can give you significant savings if you do that with the same company,” Carole Walker with Rocky Mountain Insurance said.

- Ask for discounts

Often, Insurers have loyalty discounts, senior discounts, or discounts for certain factors in your home, like a class IV hail-resistant roof.

- Update risk factors yearly

Many insurance carriers will renew a yearly policy without considering updated factors like a new roof, better security systems, or less property risk. Experts recommend letting your insurer know when you have updated something in your home that makes it safer.

“You're going to be your best advocate when it comes to saving on homeowner's insurance. Your insurance company may not know some of the things you've done recently … be talking to them about anything that can make your home a better risk,” Walker said.

- Improve your credit score

Credit score can impact your rates since insurers consider bad credit another risk. In addition, it impacts something called your “insurance score,” something that insurance underwriters consider when deciding on your rate. Insurance score is also impacted by the number of claims you make.

"The better credit you have, the lower the lower the number. the better the number and the lower the rate is. So sometimes if the husband doesn't have good credit and the wife does, we'll list the wife's name first and then, and then it can be a few hundred dollars different,” JP West with Safeco Insurance said.

- Limit small claims

Carole Walker and JP West both recommended avoiding “small claims,” or claims that barely meet your deductible. This helps improve your insurance score and keeps you from getting dropped from your policy.

- Avoid $0 claims

West also recommends not calling your insurance company for any home improvements or to come to check out your home after a major storm, as companies will log that as a claim, even if they paid nothing.

"If you call and just say, hey, can you come check out my roof, that shows up as a hail claim. And then if you say, oh, never mind, it's not enough damage or I'm going to cover it myself, it still shows up as a $0 claim and it counts against your accounts, against your claims experience,” West said.

- Consider risk factors when buying a home

Buying a home closer to a fire station impacts your risk, as your home will be closer to help in the case of an emergency. According to experts, that is also something insurance companies consider when evaluating your home for risk.

“Proximity to quality fire protection, which means how close are you to a fire station, to a hydrant? What type of fire station, What types of engine ladders do they have? How fast can they respond to your home?” Walker said. “That's something all insurance companies factor into the type of risk you are.”

West also said the age of the home you live in impacts your insurance rate since older construction homes carry higher risk as well.

- Shop around

West said that often the most effective way to get a cheaper rate is to simply switch companies.

“I had two people this morning that they were going to go from 2800 to 4000, and then we shopped around and then we're like, Oh, well, how would you like 1800?” West said.

- Increase your deductible

One of the easiest and quickest ways to ensure a cheaper rate is to raise your deductible, if you can afford it.

“Understand a higher deductible will save you short term in premiums,” Walker said. “But make sure that you can pay that amount out of pocket.”